Yes.

Here’s one of our customer’s scenarios to demonstrate how:

Sam is interested in buying a home, but has little saved for a down payment.

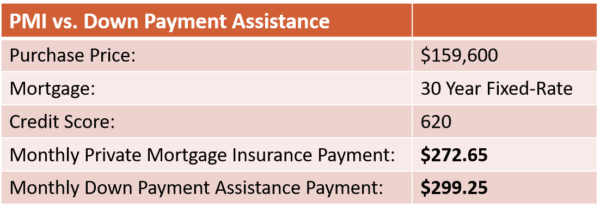

She’s found her dream house, a 3 bedroom in Rutland with a large backyard for $159,600. She’s been to her lender and is considering a mortgage for 97% of the value of the house.

Because she isn’t able to bring 20% of the value of the home to the table, her lender considers her a riskier borrower.

This means her lender adds a Private Mortgage Insurance (PMI) payment to her monthly mortgage to protect the lender in case Sam stops making payments.

Private Mortgage Insurance Protects your Lender

Sam understands why her lender considers her a riskier borrower, but she would rather not pay an insurance that doesn’t protect herself or build equity in her home. So, she considers a second option: a Down Payment Assistance Loan.

Down Payment Assistance

Sam’s heard about a Down Payment Assistance Loan from NWWVT, a second mortgage that will build equity as she pays it off and let her avoid PMI payments.

This makes her a less risky borrower to her first lender because she can now bring 20% of the purchase price to the table.

It also saves her money- she is now investing in her home with those monthly payments instead of paying Private Mortgage Insurance.

It’s like the difference between paying a landlord rent or being a homeowner– at the end of the fifteen year Down Payment Assistance Loan term, Sam will have equity built in the home that she wouldn’t have if she were paying Private Mortgage Insurance.

In Sam’s case, she’d be paying just $27 more a month, avoiding PMI, and growing equity in her home with a Down Payment Assistance Loan!

Call our Lender today and find out if Down Payment Assistance Loan makes sense for you.

Sign up for Homebuyer Education and learn all about the different loans and grants available to homebuyers!